It happens in every home remodeling project. We start the remodeling process for a lovely family, and eventually, the time comes for them to make their first large payment on either the design services or the construction work. This process is often accompanied by the question “How should we pay you?” and the intent behind that usually is: what form of payment is best, and how will the payment process be handled?

The payment process for home remodeling projects takes many forms and brings up additional questions about how payments will be made, when they will be due, and even how the project will be financed. Since these are common questions and a situation every remodeling client has to work through at some point, we’ve created this article as a resource to provide clarity for homeowners looking to work with a home remodeler in Blacksburg, VA, with questions on the financial preparation for a significant remodeling project.

For some homeowners, paying for a remodeling project with savings or investment funds is an option, which we will address further down. However, most individuals investing in a project of this size require financing, and it’s not always clear what options are available to them. In our experience, past clients use one of three financing options for remodeling projects.

The most common financing options available are the Home Equity Line of Credit (HELOC), Home Equity Loan, and the more traditional Construction Loan. Let’s review each of the three in detail, discuss the benefits and drawbacks, and explore local options for securing these types of financing.

Possibly the most popular form of financing our clients choose for their home remodel is the Home Equity Line of Credit, or “HELOC” for short. Essentially, it is a line of credit with the equity in your home providing security for the lender.

Known for its flexibility and fair terms, the HELOC allows the borrower to access a fixed amount of funds on demand. The way a HELOC works is by applying to a bank or lending institution and having an appraisal done to evaluate the equity an individual has in their home. The bank will typically grant up to a certain percentage of the equity in the home (usually capped at 80% of the owner’s equity) to the borrower in the form of a line of credit.

The funds are deposited in an account that you can access by writing checks or making draws from freely. Many individuals like the flexibility of a HELOC, which lets them access only the money they need as they need it. This process is usually done by writing checks, by wire transfer, or ACH payment from the account.

An added benefit to this process for the borrower is that they will only pay interest on the actual money borrowed. For example, if you are approved for a line of $100,000.00 but only use 10k, you will only pay interest on the 10k. Additionally, you are typically not locked into a fixed interest rate on the money borrowed. Many HELOC programs are set up with a variable interest rate, meaning you pay interest on the money you have borrowed at a rate that reflects market rates. This can be a pro and a con for borrowers, depending on what the market interest rates are doing at the time.

Perhaps the most flexible quality of the HELOC is that you can use or not use the money according to your own needs and timeline. This offers great flexibility when it comes to a home remodel or renovation project because of the expenses associated with it. Often, remodel projects are non-conforming in scheduling nature, therefore they do not follow the same parameters that a construction loan is set up for. The flexibility of a HELOC gives the borrower the power to finance a remodeling project on their own terms.

For more information about HELOC and a great option for securing one for your project, visit the National Bank of Blacksburg or another financial institution of your choice.

While we see a HELOC as the most common option for remodel financing, another option exists. The Home Equity Loan is very similar in concept to the line of credit, but a few key differences make this a better fit for some of our clients.

The main difference in the structure of these methods lies in the name. While the line of credit is on demand and can be used as needed, this loan will be disbursed in full at the time it is granted. Like a normal loan, this method is assigned a term and fixed interest rate in which you are locked into for the life of the loan, and the home is deemed as collateral within the agreement. In certain cases, and market conditions, locking in a fixed rate on your home equity loan is a great place to be in, while other less ideal economic conditions may make a variable rate more appealing.

The nature of the loan, being granted in full to the borrower at once, means this is less of a flexible spending account and more suited to expenses where you will have to pay out most of the money in a relatively short time frame, such as large upfront deposits or down payments. While both the HELOC and Home Equity Loan provide great opportunities for financing using your existing assets, they also should be taken seriously (as should all debt) because of the collateral you offer up to secure one of these loans.

The final financing option is the commonly known construction loan. While most are familiar with this in terms of new home construction, the same process can be applied to a remodeling project. These loans are set up to meet the needs of the borrower and the bank as a project progresses, and the process for releasing funds is slightly different from that of previous loan types.

The basis of a construction loan is built around the projected future value of the property. Because of this, it is in the bank’s interest, and rightfully so, not to lend money on something that does not exist yet. Because the collateral for the loan is coming to life as the construction period progresses, the bank must protect what it lends until there is a product worth lending against.

This leads to an organized inspection and sign-off process that the bank conducts as the funds are issued to the borrower and then passed through to the contractor.

Typically, Blue Ridge Design Build remodel project contracts are set up with an even, well-balanced payment schedule that is date-dependent. This method does not rely on specific scopes of work or activities being completed, but instead keeps an even and predictable payment schedule for our clients.

A construction loan payment schedule is modified to meet the requirements of the bank and typically revolves around the completion of certain project milestones. In many projects, completion of framing, mechanical systems, drywall, and final inspection are examples of approvable milestones that would be required for funds to be released and payment made.

In these situations, our team prepares a project schedule and an outline of payment milestones that reference that schedule. These invoices are sent out in accordance with work completed, and the bank then inspects and approves funds to be paid out. At the end of the construction loan period, the loan often transfers to a traditional mortgage-style agreement that is maintained for the full term of the loan.

Many of our clients have been thinking and planning their remodels for years. They have worked hard to earn and save with this project in mind and may have the opportunity to pay with “cash” or convert some of their other assets to pay for the project outright.

Let’s cover some details on how the payment process typically works.

Can I Write a Check for My Remodel Project?

As mentioned, the “how do we pay you” question really means “what form of payment works for this process”. Another common question we receive in that same conversation is, “Can we really just write a regular old check for this amount?”

It may help to paint a perspective on how the payment process is typically structured. Payments for the remodeling work are broken down by milestone dates and are relatively equal as the project progresses. For example, it’s not uncommon to have progress payments on large jobs up to $50,000 per month.

Remodeling is one of the largest investments most people will ever make, other than the purchase of their home, so it’s easy to relate to the fact that a payment of that amount is more than most are accustomed to handling.

A simple answer is that standard personal checks do work. Even though they are much less common, personal checks are still a very efficient, low-cost, and safe way to transfer funds to your home remodeler, and most of our clients use this method. Our current preference is to try to prioritize in-person exchange of written checks rather than mailing them when possible.

Some homeowners have asked whether they need to get a certified check of some sort, and the answer is no. A personal check works just fine if the account is funded to cover the amount.

One option that some clients feel more comfortable with is ordering a bank-issued check. The process typically ensures funds are available and instills confidence in the company receiving the check.

Paying For My Remodel with Wire Transfer or ACH Payment

Another common way to pay for remodel projects is through online money transfer systems like wire transfer and ACH. Specifically, when projects are paid for with personal assets, clients can more easily pay through online systems. This is especially helpful for clients who live out of town or travel often and may not be present throughout the project.

A wire transfer is a simple process that requires the exchange of account and routing information between the payor and receiver. This form of exchange is convenient but does have a fee per transfer. For example, some local options charge $30 per transfer, but this fee will vary depending on the financial institution.

ACH payments typically require a bit more setup process on the front end, but occur in a way that makes the payment fee lower per transaction. These payments can also be set up as recurring payments for the duration of the project for added convenience, if desired.

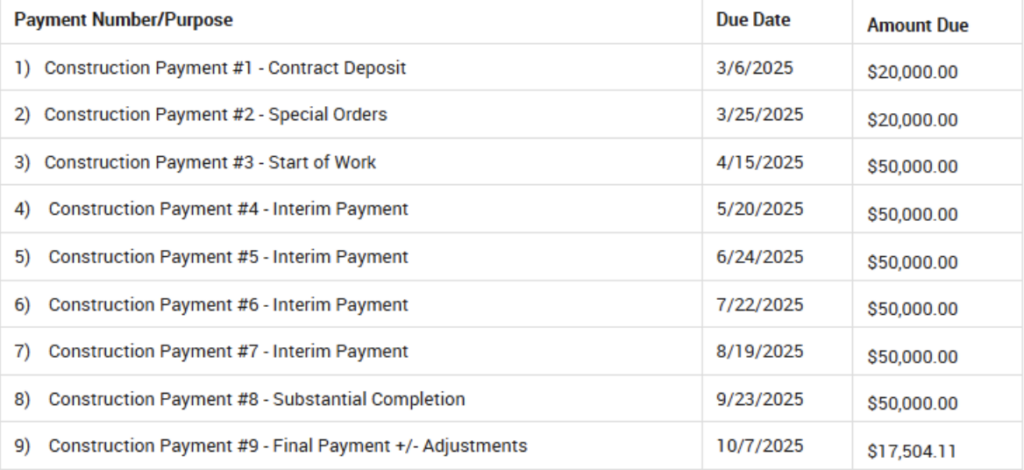

A remodeling project payment schedule is always created for each project and customized to its specific needs. The payment schedule is outlined and detailed in the construction contract for each project, but we can often provide an idea of how it will be structured, as it is normally similar across projects.

A payment schedule typically starts with a contract deposit of no more than 10% of the contract value, followed by a special orders payment at the time of long-lead time material orders. These two payments make up the first part of the payment schedule and account for all money requested prior to the start of construction to help the project get underway.

The largest portion of the project total is typically spread evenly throughout the project’s scope. For projects that are longer than six weeks, there is typically one even-sized payment per month, starting with the start of work, continuing through the interim stages, and a final large payment at the time of substantial completion.

For projects less than six weeks, it normally works well to have an even start, an interim, and a substantial completion payment. This even spacing of payments helps to keep the project funded, but also ensures payments are not ahead of the work completed.

After the project is substantially complete, a final adjustment is usually required. Because the scope of work usually contains selections and choices made during the project, these choices are reconciled at the end of the project when all billing is final. The increases and decreases are accounted for in the final payment, which is reviewed in full detail at our final walkthrough meeting before the final payment is made.

When preparing for your remodel, financial planning is something everyone must work through. Understanding the process, how payments will be made, when they will be due, and even the financing process is a great place to start and create a plan for your own situation.

While the content in this article is tailored to Blue Ridge Design Build’s remodeling process in Blacksburg, VA, it also aligns with industry standards and common financing practices.

For additional questions regarding the remodeling payment process, please call our office at (540)-951-3505 or visit BlueRidgeDesign.Build to schedule a consultation.